Roth vs. Traditional IRA: 2026 Financial Benefits for US Savers

Evaluating the Financial Benefits of Roth vs. Traditional IRAs for US Savers in 2026

As US savers look towards 2026 and beyond, making informed decisions about retirement savings vehicles becomes paramount. Among the most popular and impactful choices are the Roth IRA and the Traditional IRA. While both offer significant tax advantages for retirement planning, their mechanics and benefits differ substantially, catering to distinct financial situations and future outlooks. Understanding the nuances of Roth vs Traditional IRA is not merely an academic exercise; it’s a critical step in optimizing your long-term financial health.

This comprehensive guide aims to dissect the intricacies of both Roth and Traditional IRAs, providing US savers with the knowledge necessary to determine which option, or combination thereof, best suits their individual circumstances in 2026. We will delve into their core functionalities, tax implications for contributions and withdrawals, eligibility requirements, and how various life stages and financial projections influence the optimal choice. By the end of this article, you will be equipped to evaluate the financial benefits of Roth vs. Traditional IRAs with confidence, ensuring your retirement savings strategy is as robust and efficient as possible.

The landscape of retirement planning is ever-evolving, with tax laws, economic conditions, and individual financial goals constantly shifting. For US savers, the choice between a Roth IRA and a Traditional IRA is often one of the most significant financial decisions they will make. This decision hinges largely on one fundamental question: do you prefer to pay taxes now or later? The answer to this question, however, is rarely simple and requires a thorough understanding of your current income, anticipated future income, and overall financial strategy. Let’s embark on a detailed exploration of these two powerful retirement tools, focusing on their relevance and benefits for US savers in 2026.

Understanding the Traditional IRA: Tax Deductions Today

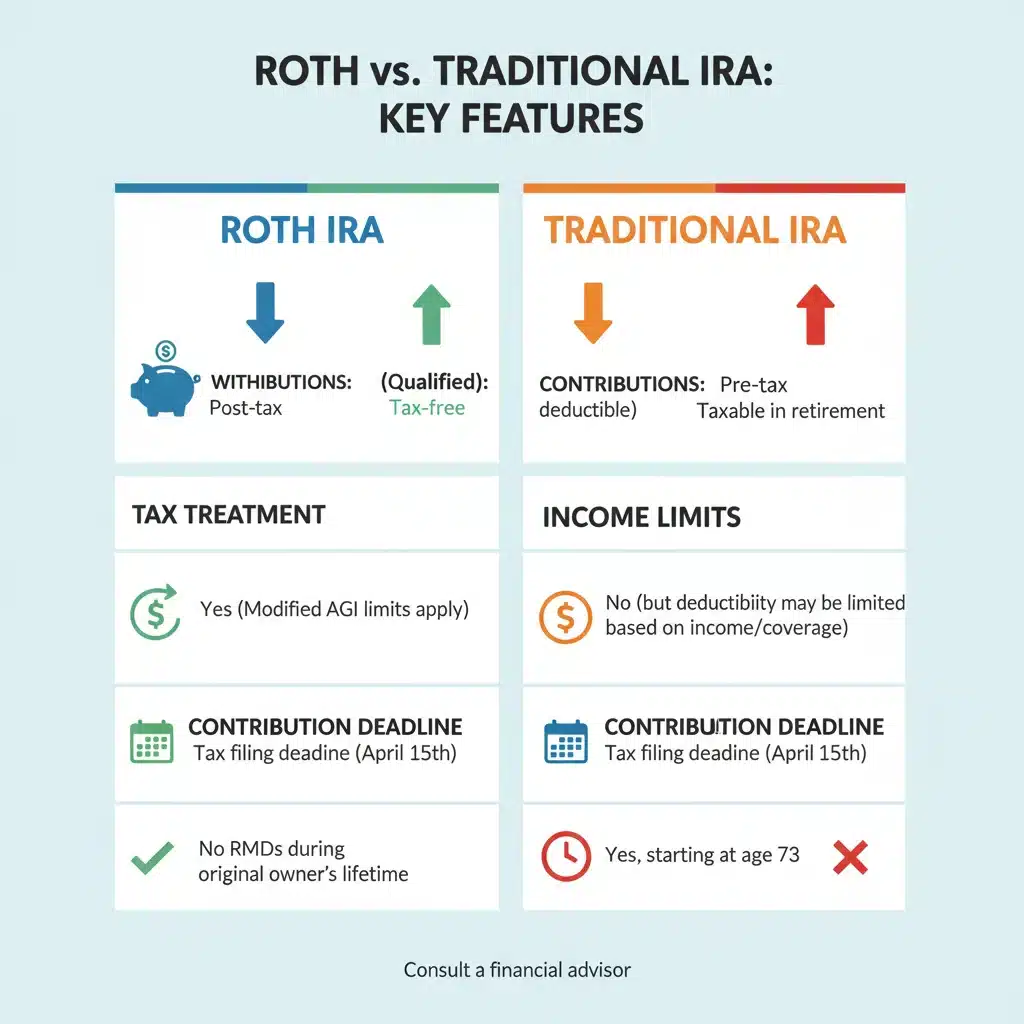

The Traditional IRA has been a cornerstone of American retirement planning for decades, offering immediate tax benefits to eligible individuals. When you contribute to a Traditional IRA, your contributions are often tax-deductible in the year they are made. This means that if you contribute $6,500 (assuming current limits, adjusted for 2026) to a Traditional IRA, and you’re in the 22% tax bracket, you could potentially reduce your taxable income by $6,500, leading to a tax saving of $1,430. This upfront tax deduction is a significant draw for many US savers, particularly those who anticipate being in a lower tax bracket during retirement.

How Traditional IRAs Work: Contributions and Growth

Contributions to a Traditional IRA grow tax-deferred. This means that you don’t pay taxes on any investment gains, dividends, or interest until you withdraw the money in retirement. This tax-deferred growth allows your investments to compound more aggressively over time, as your earnings are reinvested without being diminished by annual taxes. For example, if your investments generate 7% annual returns, and you don’t pay taxes on those returns until retirement, the power of compounding works wonders for your nest egg.

Withdrawals in Retirement: The Taxable Event

The primary trade-off for the upfront tax deduction and tax-deferred growth is that withdrawals from a Traditional IRA in retirement are generally taxed as ordinary income. This is where the expectation of future tax brackets comes into play. If you anticipate being in a lower tax bracket during retirement than you are in your working years, a Traditional IRA can be an incredibly efficient way to save. You get a tax break when your income is higher, and you pay taxes when your income (and presumably your tax bracket) is lower. However, if your tax bracket remains the same or increases in retirement, the benefit of the upfront deduction might be diluted.

Eligibility and Deductibility Rules for 2026

For 2026, eligibility for contributing to a Traditional IRA remains quite broad, with no income limits for contributions. However, the deductibility of your contributions can be affected by whether you or your spouse are covered by a retirement plan at work. If neither you nor your spouse is covered by a workplace retirement plan, your Traditional IRA contributions are fully deductible, regardless of your income. If you are covered by a workplace plan, the deductibility of your contributions phases out at higher income levels. It’s crucial for US savers to stay updated on the specific income thresholds and contribution limits for 2026, as these figures are subject to annual adjustments by the IRS. Understanding these rules is essential for maximizing the benefits of your Roth vs Traditional IRA decision.

Exploring the Roth IRA: Tax-Free Withdrawals Later

The Roth IRA, introduced in 1997, offers a contrasting yet equally powerful approach to retirement savings: tax-free withdrawals in retirement. This benefit comes with a different tax treatment during the contribution phase. Contributions to a Roth IRA are made with after-tax dollars, meaning you don’t get an upfront tax deduction. However, this initial sacrifice pays off handsomely in retirement.

How Roth IRAs Work: After-Tax Contributions and Tax-Free Growth

Unlike Traditional IRAs, your contributions to a Roth IRA are made with money that has already been taxed. The magic of a Roth IRA lies in its growth and withdrawals. All qualified withdrawals from a Roth IRA in retirement are completely tax-free. This includes your original contributions and all the earnings your investments have accumulated over the years. This feature is particularly attractive to US savers who anticipate being in a higher tax bracket in retirement than they are today.

The Power of Tax-Free Income in Retirement

Imagine a scenario where your Roth IRA has grown significantly over several decades. When you retire, you can withdraw all of that money – both your initial contributions and the substantial investment gains – without paying a single cent in federal income tax. This can be an enormous advantage, especially as tax rates may increase in the future. For US savers, the certainty of tax-free income in retirement provides invaluable peace of mind and simplifies financial planning in later years. This characteristic is a major differentiator in the Roth vs Traditional IRA debate.

Eligibility and Income Limits for 2026

While Roth IRAs offer incredible tax benefits, they do come with income limitations for direct contributions. For 2026, individuals and married couples filing jointly will have specific Modified Adjusted Gross Income (MAGI) thresholds that determine their eligibility to contribute directly to a Roth IRA. These limits are typically adjusted annually for inflation. If your income exceeds these thresholds, you may not be able to contribute directly to a Roth IRA. However, there are strategies like the ‘backdoor Roth IRA’ that allow higher-income earners to contribute indirectly, navigating these limits. Understanding these income restrictions is crucial when considering your Roth vs Traditional IRA options.

Key Differences and Considerations for US Savers in 2026

The fundamental distinction between a Roth IRA and a Traditional IRA boils down to when you receive your tax break: now or later. However, several other factors play a significant role in determining which option is best for your specific situation. Let’s explore these critical differences.

Tax Treatment of Contributions and Withdrawals

This is the most apparent difference. Traditional IRA contributions might be tax-deductible, leading to tax-deferred growth and taxable withdrawals in retirement. Roth IRA contributions are not tax-deductible, but qualified withdrawals in retirement are entirely tax-free. Your current and projected future tax bracket is the primary driver in this decision. If you expect your tax bracket to be higher in retirement, a Roth IRA is generally more advantageous. If you anticipate a lower tax bracket in retirement, a Traditional IRA might be more beneficial.

Income Limits and Eligibility

Traditional IRAs have no income limits for contributions, though deductibility can be phased out based on income and workplace retirement plan coverage. Roth IRAs, conversely, have MAGI limits for direct contributions, which can be a hurdle for high-income earners. This difference is vital for US savers to consider, especially if their income is close to or exceeds the Roth IRA income thresholds for 2026.

Required Minimum Distributions (RMDs)

Traditional IRAs are subject to Required Minimum Distributions (RMDs) once you reach a certain age (currently 73, but this could be adjusted for 2026 and beyond by legislative changes). This means you must start withdrawing a minimum amount from your Traditional IRA each year, regardless of whether you need the money. Roth IRAs, for the original owner, do not have RMDs. This flexibility can be a significant advantage, allowing your money to continue growing tax-free for as long as you wish, and offering greater control over your retirement income stream. This RMD difference can heavily influence the Roth vs Traditional IRA choice for estate planning.

Flexibility and Early Withdrawals

Roth IRAs offer unique flexibility regarding early withdrawals. You can withdraw your original contributions from a Roth IRA at any time, for any reason, tax-free and penalty-free. This is because you’ve already paid taxes on these contributions. This feature can act as a valuable emergency fund or a source of funds for other significant life events without incurring penalties or taxes, unlike a Traditional IRA. While it’s generally not advisable to dip into retirement savings, this flexibility can be a comforting safety net. This flexibility is a strong point for the Roth in the Roth vs Traditional IRA debate for younger savers.

Contribution Limits for 2026

Both Roth and Traditional IRAs typically share the same annual contribution limits, which are adjusted periodically for inflation. For 2026, these limits will likely be slightly higher than current figures. It’s crucial to be aware of these limits and maximize your contributions to either account to fully capitalize on their respective benefits. Staying informed about the latest IRS guidelines is key for all US savers.

When to Choose a Roth IRA for 2026

For many US savers, a Roth IRA will be the more advantageous choice, especially if certain conditions apply to their financial situation in 2026:

-

You expect to be in a higher tax bracket in retirement: If you are currently in a lower tax bracket (e.g., early in your career, or taking a career break), but anticipate earning more and moving into a higher tax bracket later in life or in retirement, the Roth IRA is highly beneficial. Paying taxes now at a lower rate to enjoy tax-free withdrawals later is a powerful strategy.

-

You are young and have a long time horizon: The longer your money has to grow tax-free, the more significant the benefit of a Roth IRA becomes. The compounding effect on tax-free earnings over several decades can result in a substantial tax savings in retirement.

-

You want tax-free income in retirement: The certainty of tax-free withdrawals provides predictable retirement income, which can be invaluable for budgeting and financial planning in your later years. This also protects you from potential future tax rate increases.

-

You want flexibility for early withdrawals (of contributions): The ability to withdraw your original contributions without tax or penalty offers a valuable layer of financial flexibility that a Traditional IRA does not provide.

-

You want to avoid RMDs: If you prefer to have complete control over when and how much you withdraw from your retirement accounts, and wish to avoid forced distributions, a Roth IRA is superior as it has no RMDs for the original owner.

-

You are a high-income earner using the ‘backdoor Roth’ strategy: Even if your income exceeds the direct contribution limits, the ‘backdoor Roth’ strategy allows you to contribute to a non-deductible Traditional IRA and then convert it to a Roth IRA. This is a popular strategy for affluent US savers who still want the benefits of a Roth.

Considering these points helps clarify the Roth vs Traditional IRA decision for many.

When to Choose a Traditional IRA for 2026

Despite the allure of tax-free withdrawals, a Traditional IRA remains an excellent choice for many US savers, particularly those who fit the following profiles in 2026:

-

You expect to be in a lower tax bracket in retirement: If you are currently in a high tax bracket and anticipate your income (and thus your tax bracket) to decrease significantly in retirement, the immediate tax deduction offered by a Traditional IRA is highly attractive. You get a tax break when you need it most and pay taxes when your income is lower.

-

You want an immediate tax deduction: The upfront tax savings can be used to reduce your current tax liability, which can free up funds for other financial goals or simply boost your take-home pay today. This immediate benefit is a powerful incentive for many to choose a Traditional IRA.

-

You are trying to lower your Adjusted Gross Income (AGI): Contributing to a deductible Traditional IRA can lower your AGI, which can have ripple effects on your eligibility for other tax credits, deductions, or even lower your Medicare premiums in retirement.

-

You are not eligible for a Roth IRA due to income limits: If your income exceeds the MAGI limits for direct Roth IRA contributions and you do not wish to use the backdoor Roth strategy, a Traditional IRA provides a valuable alternative for tax-advantaged retirement savings.

-

You already have a significant amount of tax-free income planned for retirement: If you expect to have substantial tax-free income from other sources (e.g., Roth 401(k), tax-free investments), diversifying with a Traditional IRA can provide a different tax profile for your retirement income streams.

The upfront tax benefits of a Traditional IRA are a powerful argument in the Roth vs Traditional IRA debate for those with higher current incomes.

The Hybrid Approach: Leveraging Both Roth and Traditional IRAs

It’s important to remember that the choice between Roth vs Traditional IRA is not always an either/or proposition. Many US savers find that a hybrid approach, contributing to both types of IRAs, offers the most robust and flexible retirement strategy. This allows you to hedge against future tax uncertainty and diversify your tax exposure in retirement.

Diversifying Your Tax Portfolio

By contributing to both a Roth and a Traditional IRA, you create a diversified ‘tax portfolio’ for your retirement. Some of your retirement income will be tax-free (from the Roth), and some will be taxable (from the Traditional). This gives you immense flexibility in retirement to manage your taxable income. For instance, in years when you need more income, you can strategically withdraw from your Roth IRA to keep your taxable income lower, potentially avoiding higher tax brackets or reducing the impact on Social Security taxation.

Adapting to Changing Circumstances

Your financial situation, tax bracket, and retirement goals can change over time. Starting with one type of IRA doesn’t mean you’re locked in forever. You can adjust your contributions annually based on your evolving circumstances. For example, if you’re in a lower tax bracket early in your career, you might prioritize a Roth IRA. As your income grows and you enter a higher tax bracket, you might shift some contributions to a Traditional IRA to take advantage of the immediate tax deduction. This adaptability is a key advantage of understanding the interplay between Roth vs Traditional IRA.

Important Considerations for US Savers in 2026

Beyond the core differences, several other factors should influence your Roth vs Traditional IRA decision for 2026:

Future Tax Rates and Legislation

Predicting future tax rates is impossible, but it’s a critical factor in the Roth vs. Traditional IRA decision. If you believe tax rates are likely to increase in the future (perhaps due to national debt or demographic shifts), a Roth IRA becomes more appealing because you lock in your tax rate today. Conversely, if you expect tax rates to decrease, a Traditional IRA might seem more attractive. Staying informed about potential legislative changes affecting retirement accounts is vital for US savers.

Estate Planning Implications

Roth IRAs can be powerful estate planning tools. Because they have no RMDs for the original owner, the funds can continue to grow tax-free throughout your lifetime. Upon your death, your beneficiaries can inherit the Roth IRA and continue to take tax-free withdrawals (though they may be subject to RMDs themselves, depending on their relationship to you and the specific rules in place). Traditional IRAs, on the other hand, typically require beneficiaries to pay income tax on withdrawals. This difference can significantly impact the legacy you leave behind.

Impact on Other Retirement Accounts

Your IRA choice should also be considered in the context of your other retirement savings, such as a 401(k), 403(b), or 457 plan. Many workplace plans now offer Roth 401(k) options. If you contribute to a Roth 401(k), you might choose a Traditional IRA to diversify your tax treatment. Conversely, if your workplace plan is entirely pre-tax (Traditional), adding a Roth IRA can provide valuable tax-free income in retirement. A holistic view of all your retirement accounts is essential for an optimal strategy.

Inflation and Purchasing Power

While both IRAs help combat inflation through investment growth, the tax treatment impacts your net purchasing power in retirement. Tax-free withdrawals from a Roth IRA mean that the entire amount you withdraw is available to spend, potentially offering greater certainty in budgeting against inflation. With a Traditional IRA, you must factor in the tax bite, which can reduce your effective purchasing power if tax rates are higher than anticipated.

Making Your Decision for 2026

The choice between a Roth and Traditional IRA for US savers in 2026 is deeply personal and depends on a multitude of factors, including your current income, projected future income, age, risk tolerance, and overall financial goals. There is no one-size-fits-all answer, and what works for one individual may not be ideal for another. The critical step is to carefully evaluate your own financial landscape and make an informed decision.

Consult a Financial Advisor

Given the complexity of tax laws and individual financial situations, consulting a qualified financial advisor is highly recommended. A professional can help you analyze your specific circumstances, project future tax scenarios, and guide you towards the most advantageous Roth vs Traditional IRA strategy for your 2026 retirement planning and beyond. They can also help you navigate potential income limits, backdoor Roth strategies, and the interplay with other retirement accounts.

Stay Informed About Legislative Changes

Retirement account rules and tax laws are subject to change. Staying informed about potential legislative updates from the IRS and Congress is crucial. These changes can impact contribution limits, income thresholds, RMD rules, and other aspects that could sway your Roth vs Traditional IRA decision. Reliable financial news sources and your financial advisor can help you stay abreast of these developments.

Regularly Review Your Strategy

Retirement planning is not a one-time event. It’s an ongoing process. As your income changes, your family situation evolves, or tax laws shift, it’s wise to regularly review your retirement savings strategy. What was the best choice for you in 2026 might not be the optimal choice in 2029 or 2035. Periodically reassessing your Roth vs Traditional IRA allocations ensures your plan remains aligned with your long-term goals.

Conclusion: Optimizing Your Retirement Future

The debate between Roth vs Traditional IRA is a cornerstone of effective retirement planning for US savers. Both offer powerful mechanisms to save for the future with significant tax advantages, but they cater to different tax philosophies and financial realities. The Traditional IRA provides immediate tax relief and tax-deferred growth, ideal for those who anticipate lower tax brackets in retirement. The Roth IRA, with its after-tax contributions and tax-free withdrawals, is a powerhouse for individuals who expect higher tax brackets in their golden years or desire tax-free income certainty.

For 2026 and the years to come, understanding these distinctions is not just beneficial; it’s essential for maximizing your retirement nest egg. Whether you choose one over the other, or adopt a hybrid approach, the key is to make an intentional decision based on a thorough analysis of your unique financial situation. By doing so, US savers can confidently navigate the complexities of retirement planning and build a secure and prosperous future.

Contribution Limits: Maximize Your Retirement Savings")

Limits & Smart Moves")

Contributions 2025: Maximize Your Growth")