US Housing Market Predictions 2026: Navigating 7% Mortgage Rates

US Housing Market Predictions for 2026: Financial Strategies for Buyers and Sellers Amidst 7% Mortgage Rates

The United States housing market is a dynamic and ever-evolving landscape, constantly influenced by a myriad of economic factors, demographic shifts, and global events. As we cast our gaze forward to 2026, one of the most prominent factors shaping the future of real estate appears to be the trajectory of mortgage interest rates. With projections hinting at rates potentially stabilizing around the 7% mark, both prospective buyers and current homeowners looking to sell are bracing for a significantly different market environment than what has been experienced in recent years. Understanding these US Housing 2026 predictions is not just about anticipating challenges; it’s about identifying opportunities and crafting robust financial strategies to navigate a potentially complex, yet rewarding, real estate journey.

The journey to 2026 will undoubtedly be paved with economic adjustments. Inflationary pressures, the Federal Reserve’s monetary policy, and broader economic growth will all play pivotal roles in determining the precise path of mortgage rates. A 7% mortgage rate, while higher than the historically low rates seen during the pandemic, is still within the realm of historical averages. However, its impact on affordability, particularly in a market that has seen substantial price appreciation, cannot be overstated. This article aims to provide a comprehensive overview of the anticipated landscape, offering actionable insights and financial strategies for those looking to enter or exit the US Housing 2026 market.

Understanding the Economic Landscape Leading to 2026

Before delving into specific strategies, it’s crucial to grasp the economic forces that are likely to shape the US Housing 2026 market. Several key indicators will influence mortgage rates and housing demand:

Inflation and Federal Reserve Policy

Inflation has been a dominant theme in recent years, prompting the Federal Reserve to implement aggressive interest rate hikes. While the Fed does not directly set mortgage rates, its policy decisions significantly influence the federal funds rate, which in turn impacts the cost of borrowing across the economy, including mortgage rates. By 2026, it is anticipated that inflation will have moderated closer to the Fed’s target of 2%. However, the path to this target is not linear. Any resurgence in inflationary pressures could lead to the Fed maintaining a tighter monetary policy, keeping mortgage rates elevated. Conversely, a more rapid decline in inflation could provide some leeway for rates to dip, though a return to sub-4% rates is highly improbable.

Economic Growth and Employment

A robust economy with strong employment figures typically supports a healthy housing market. When people are employed and feel secure in their jobs, they are more likely to invest in homeownership. However, sustained high interest rates can cool economic growth, potentially leading to a slowdown in job creation. The balance between combating inflation and fostering economic growth will be a delicate act for policymakers, directly affecting consumer confidence and the willingness to undertake a significant financial commitment like a home purchase in US Housing 2026.

Supply and Demand Dynamics

The fundamental principles of supply and demand remain critical. The US has faced a persistent housing supply shortage for years, a factor that has underpinned price appreciation even during periods of higher rates. Construction activity, labor availability, and material costs will all influence the pace at which new homes enter the market. If supply continues to lag behind demand, home prices may remain resilient, even with higher mortgage rates, further exacerbating affordability challenges. Conversely, a significant increase in housing starts could alleviate some pressure, creating a more balanced market for US Housing 2026 participants.

Impact of 7% Mortgage Rates on Buyers

For prospective homebuyers, a 7% mortgage rate presents both challenges and a need for strategic adjustments. The most immediate impact will be on affordability and purchasing power.

Reduced Affordability and Purchasing Power

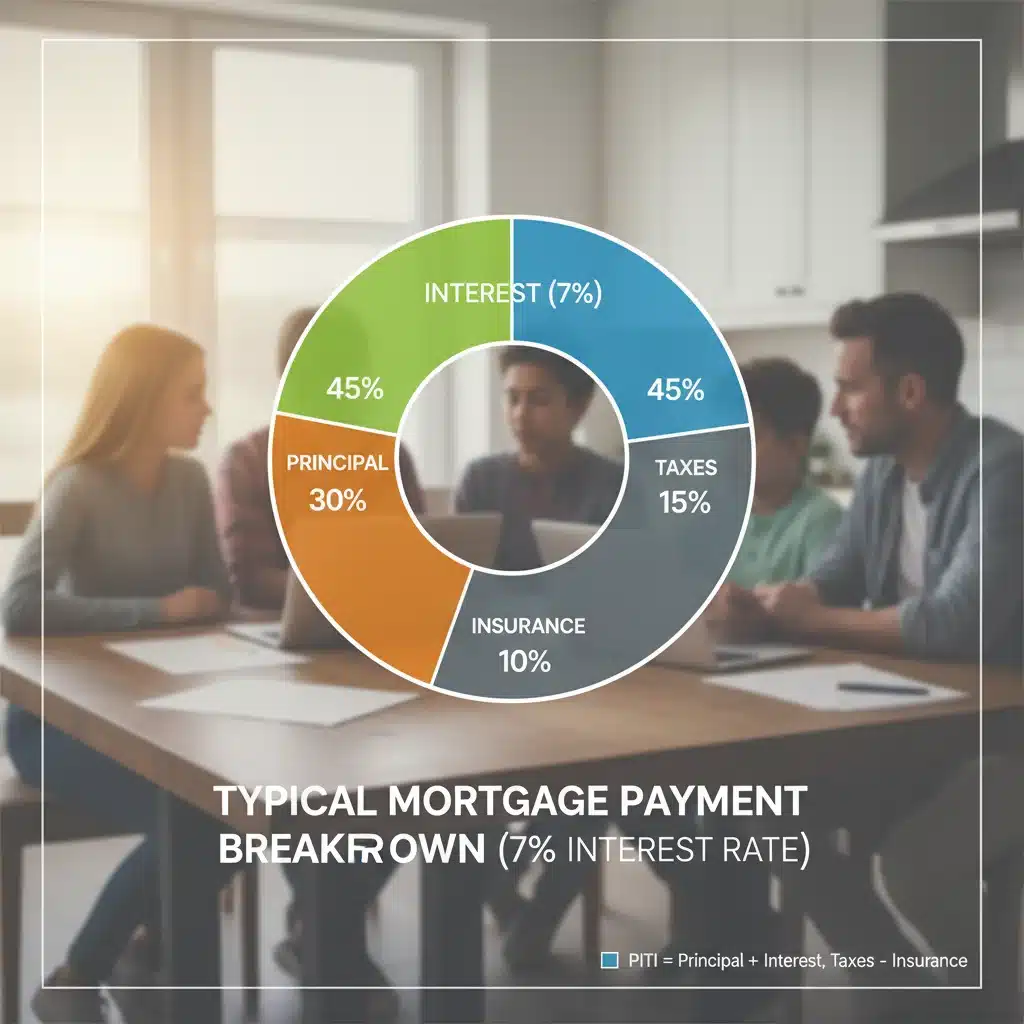

Higher interest rates mean a larger portion of a monthly mortgage payment goes towards interest, reducing the principal repayment and increasing the overall cost of borrowing. This directly translates to reduced purchasing power. A buyer who could afford a $400,000 home at a 3% interest rate might only be able to afford a $300,000 home at a 7% rate, assuming the same monthly payment. This will necessitate a recalibration of expectations for many, potentially leading to:

- Looking at smaller homes or homes in less desirable (and thus, less expensive) neighborhoods.

- Delaying homeownership to save a larger down payment.

- Considering alternative financing options or adjustable-rate mortgages (ARMs), though with careful consideration of associated risks.

Increased Focus on Financial Preparedness

In a 7% interest rate environment, strong financial health becomes even more paramount. Lenders will likely scrutinize credit scores, debt-to-income ratios, and savings more closely. Buyers should prioritize:

- Improving credit scores to secure the best possible rates.

- Reducing existing debt to lower their debt-to-income ratio.

- Amassing a substantial down payment to reduce the loan amount and, consequently, the monthly payment.

- Building a robust emergency fund to withstand unexpected financial shocks.

Strategies for Buyers in US Housing 2026

Despite the challenges, opportunities still exist for determined buyers. Here are some key strategies:

1. Prioritize Savings and Down Payment

A larger down payment directly reduces the loan amount, making monthly payments more manageable even with higher interest rates. Aim for 20% or more to avoid private mortgage insurance (PMI) and secure better loan terms. Explore first-time homebuyer programs or down payment assistance programs, which can be invaluable resources.

2. Explore Adjustable-Rate Mortgages (ARMs) with Caution

ARMs often start with lower interest rates for an initial fixed period (e.g., 5/1 or 7/1 ARM) before adjusting periodically. This can be attractive in a high-rate environment, especially if you anticipate refinancing when rates drop or selling before the fixed period ends. However, the risk of rates increasing significantly after the fixed period must be carefully weighed. Consult with a financial advisor to understand the potential implications.

3. Focus on "Fixer-Uppers" or Less Competitive Markets

Homes requiring some renovation might be priced lower, offering an entry point into homeownership. Similarly, exploring emerging markets or less saturated areas can yield more affordable options. Be prepared to invest time and resources into these properties.

4. Get Pre-Approved and Understand Your Budget

Getting pre-approved for a mortgage provides a clear understanding of what you can truly afford. It also signals to sellers that you are a serious and qualified buyer, which can be an advantage in a competitive market. Work with a reputable lender to explore all available loan products and understand the total cost of ownership, including property taxes, insurance, and potential HOA fees.

5. Be Patient and Strategic

The US Housing 2026 market may not be characterized by rapid price appreciation seen in previous years. Patience can be a virtue. Take your time to find the right property that aligns with your budget and long-term goals. Don’t rush into a purchase out of fear of missing out; instead, make informed decisions.

Impact of 7% Mortgage Rates on Sellers

For homeowners looking to sell, a 7% mortgage rate environment means a shift in market dynamics. The seller’s market of recent years, characterized by bidding wars and waived contingencies, may cool, requiring a more strategic approach.

Longer Time on Market and Price Adjustments

With higher borrowing costs, fewer buyers will be able to afford top-tier prices. This will likely lead to homes spending more time on the market. Sellers may need to be more flexible with pricing, potentially adjusting their asking price downwards to attract buyers. Overpricing a home in this environment can lead to stagnation and eventually a more significant price reduction.

Increased Importance of Home Condition and Presentation

In a market where buyers have more options and are facing higher financing costs, they will be more discerning. Homes that are move-in ready, well-maintained, and aesthetically pleasing will stand out. Sellers should invest in minor repairs, decluttering, staging, and professional photography to make their property as appealing as possible.

Fewer Bidding Wars and More Contingencies

The era of multiple offers and waived contingencies might become less common. Buyers, facing higher interest rates, will likely reintroduce contingencies for inspections, appraisals, and financing. Sellers should be prepared for more negotiation and potentially longer closing periods.

Strategies for Sellers in US Housing 2026

Sellers can still achieve successful outcomes by adopting a proactive and realistic approach:

1. Price Competitively from the Outset

Working with an experienced real estate agent to conduct a thorough comparative market analysis (CMA) is crucial. Pricing your home realistically and competitively from day one can prevent it from sitting on the market, which often leads to eventual deeper price cuts. Understand that the market has shifted, and past sales prices may not be indicative of current value.

2. Invest in Pre-Sale Preparations

Minor renovations, fresh paint, updated fixtures, and professional staging can significantly enhance your home’s appeal. Focus on areas that offer the highest return on investment, such as kitchens and bathrooms. A well-prepared home justifies its asking price and attracts serious buyers.

3. Be Flexible and Open to Negotiation

Be prepared to negotiate on price, contingencies, and even seller concessions (e.g., contributing to closing costs or offering a rate buy-down). A willingness to be flexible can be the difference between a sale and a prolonged listing.

4. Highlight Unique Selling Propositions (USPs)

Emphasize what makes your home unique – energy-efficient features, a desirable school district, smart home technology, or a beautifully landscaped yard. These USPs can help your home stand out in a more competitive market.

5. Consider a "Rate Buy-Down" for Buyers

As a seller, you might consider offering to pay points to "buy down" the buyer’s interest rate for the first year or two of their loan. This can make your home more appealing by reducing the buyer’s initial monthly payments, effectively making their purchase more affordable without significantly reducing your asking price.

Investment Perspectives in the US Housing 2026 Market

For real estate investors, a 7% mortgage rate environment necessitates a re-evaluation of strategies. While the "easy money" of low-interest rates may be gone, new opportunities can emerge for savvy investors.

Cash Flow Over Appreciation

In a higher-rate environment, the focus for rental property investors will likely shift from rapid capital appreciation to strong cash flow. Properties that can generate consistent rental income that comfortably covers mortgage payments, taxes, insurance, and maintenance will be highly desirable. Investors will need to perform rigorous due diligence on potential rental yields and operating expenses.

Focus on Value-Add Opportunities

Properties that require renovation or have untapped potential will offer better returns. Investors who can add value through strategic upgrades, conversions, or property management improvements can create equity and increase rental income, offsetting the impact of higher borrowing costs.

Diversification and Geographic Considerations

Diversifying investment portfolios across different property types (single-family, multi-family, commercial) and geographic locations can mitigate risks. Some regions may experience stronger economic growth or more favorable supply/demand dynamics, making them more attractive for investment in US Housing 2026.

Build-to-Rent and Institutional Investors

The build-to-rent sector may continue to see growth, as higher mortgage rates push more individuals towards renting. Institutional investors, with access to cheaper capital or different financing structures, may continue to be active in this space, potentially competing with individual investors for certain property types.

Long-Term Outlook and Adaptability

The US Housing 2026 market, shaped by 7% mortgage rates, will demand adaptability from all participants. While the immediate focus is on managing the impact of higher rates, it’s also important to consider the long-term implications and opportunities.

The "New Normal" for Mortgage Rates

It’s possible that 7% mortgage rates, or rates in a similar range, could become the "new normal" after a period of historically low rates. This would necessitate a fundamental shift in how affordability is calculated and how real estate investments are evaluated. Consumers and investors alike will need to adjust their expectations and financial models accordingly.

Technological Advancements and Data-Driven Decisions

The role of technology in real estate will continue to expand. Data analytics, AI-powered insights, and virtual reality tours will become even more crucial for making informed decisions. Buyers and sellers who leverage these tools will have a competitive advantage in navigating the complexities of the US Housing 2026 market.

Sustainability and Green Building

Increasing awareness of climate change and energy costs will likely drive demand for sustainable and energy-efficient homes. Properties with green features may command a premium, and investors who focus on these types of developments could see long-term benefits. Government incentives for energy-efficient upgrades could also influence market trends.

Demographic Shifts

Demographic trends, such as the aging population, the rise of remote work, and migration patterns, will continue to influence housing demand in specific regions. Understanding these shifts can help both buyers and sellers identify areas of growth or decline, informing their strategies for the US Housing 2026 market.

Conclusion: Navigating the Future of US Housing

The US Housing 2026 market, with its anticipated 7% mortgage rates, will undoubtedly present a different set of challenges and opportunities compared to the recent past. For buyers, it will demand greater financial discipline, a willingness to adjust expectations, and a strategic approach to finding affordable options. For sellers, it will require competitive pricing, meticulous home preparation, and flexibility in negotiations. For investors, the focus will shift towards cash flow, value-add opportunities, and careful market analysis.

The key to success in this evolving landscape lies in informed decision-making, adaptability, and a long-term perspective. Engaging with experienced real estate professionals, financial advisors, and lenders will be more critical than ever. By understanding the underlying economic forces, preparing financially, and employing strategic approaches, both buyers and sellers can confidently navigate the future of the US Housing 2026 market and achieve their real estate goals. The market is not collapsing; it’s recalibrating, and those who adapt will thrive.

Ultimately, the resilience of the US housing market is rooted in fundamental demand for shelter and the desire for homeownership. While the road to 2026 might be bumpier due to higher interest rates, the underlying drivers remain strong. Those who approach the market with careful planning and a clear understanding of the new dynamics will be well-positioned for success.