2026 Social Security COLA: What Retirees Need to Know for Retirement Planning

Understanding the 2026 Social Security Cost-of-Living Adjustment (COLA) and Your Retirement Planning

As we navigate the complexities of financial planning, few topics hold as much significance for retirees and those nearing retirement as Social Security. Central to this discussion is the annual Cost-of-Living Adjustment, or COLA. Specifically, understanding the 2026 Social Security COLA is paramount for effective retirement planning. This comprehensive guide will delve into what COLA is, how it’s calculated, its historical trends, and crucially, how the 2026 adjustment might impact your financial future.

What is the Social Security COLA?

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security and Supplemental Security Income (SSI) benefits to offset the effects of inflation. Its primary purpose is to ensure that the purchasing power of Social Security benefits doesn’t erode over time due to rising prices of goods and services. Without COLA, the fixed income of retirees would steadily lose value, making it increasingly difficult to meet basic living expenses.

The concept of COLA was introduced in 1975, following amendments to the Social Security Act in 1972. Before this, benefit increases required an act of Congress. The automatic COLA mechanism was designed to provide a more consistent and predictable adjustment, directly linking benefit increases to inflation. This change was a significant step towards protecting the financial stability of millions of Americans relying on Social Security.

The adjustment is typically announced in October each year and takes effect in December, with the increased benefits appearing in January payments. Therefore, while we are discussing the 2026 Social Security COLA, the official announcement will come in October 2025, based on inflation data leading up to that point.

How is the 2026 Social Security COLA Calculated?

The calculation of the Social Security COLA is a precise process overseen by the Social Security Administration (SSA). It’s based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). The CPI-W is one of several consumer price indices published by the Bureau of Labor Statistics (BLS) and is specifically chosen because it reflects the spending patterns of working-class Americans, who are often the beneficiaries of Social Security.

Here’s a breakdown of the calculation methodology:

- Reference Period: The SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the most recent year in which a COLA was payable.

- Percentage Increase: The percentage increase in the CPI-W between these two periods determines the COLA. For example, to determine the 2026 Social Security COLA, the SSA will compare the average CPI-W for Q3 2025 with the average CPI-W for Q3 2024 (assuming a COLA was payable in 2025).

- Rounding: The calculated percentage increase is then rounded to the nearest one-tenth of one percent.

- Zero COLA: If there is no increase in the CPI-W, or if it decreases, there is no COLA. This has occurred a few times in history, during periods of deflation or very low inflation.

It’s important to note that the CPI-W differs from the more commonly cited Consumer Price Index for All Urban Consumers (CPI-U). The CPI-U covers a broader population, including professionals, self-employed individuals, and retirees, while the CPI-W focuses on wage earners and clerical workers. Critics often argue that the CPI-W doesn’t accurately reflect the spending habits of seniors, who typically spend a larger proportion of their income on healthcare and housing, which often inflate at higher rates than other goods and services. This discrepancy can lead to a perceived inadequacy in COLA adjustments for some retirees.

Factors Influencing the 2026 Social Security COLA

Several economic factors will play a crucial role in determining the 2026 Social Security COLA. Understanding these influences can help you anticipate potential adjustments and refine your retirement planning.

- Inflation Rates: The most direct determinant is the rate of inflation, particularly as measured by the CPI-W. Sustained increases in the prices of gasoline, food, housing, and other consumer goods will push the CPI-W higher, leading to a larger COLA. Conversely, a slowdown in inflation or deflationary pressures would result in a smaller or even zero COLA.

- Economic Growth: A robust economy with strong consumer demand can lead to higher inflation, as businesses may raise prices to meet demand. Conversely, an economic downturn could temper inflation and, consequently, COLA.

- Energy Prices: Fluctuations in oil and gas prices have a significant impact on the CPI-W. Higher energy costs directly affect transportation and production costs, which then filter down to consumer prices.

- Food Prices: As a fundamental necessity, food prices are a substantial component of the CPI-W. Volatility in agricultural markets, supply chain disruptions, or adverse weather conditions can drive food inflation.

- Housing Costs: Rent and homeownership costs are also significant factors. Rising housing expenses contribute substantially to the overall inflation picture and, thus, to the COLA calculation.

- Global Events: Geopolitical events, international trade policies, and global supply chain disruptions can all have ripple effects on domestic inflation and, by extension, the COLA.

Forecasting the 2026 Social Security COLA involves analyzing these complex and interconnected economic indicators. While precise predictions are difficult, staying informed about economic trends can provide valuable insights.

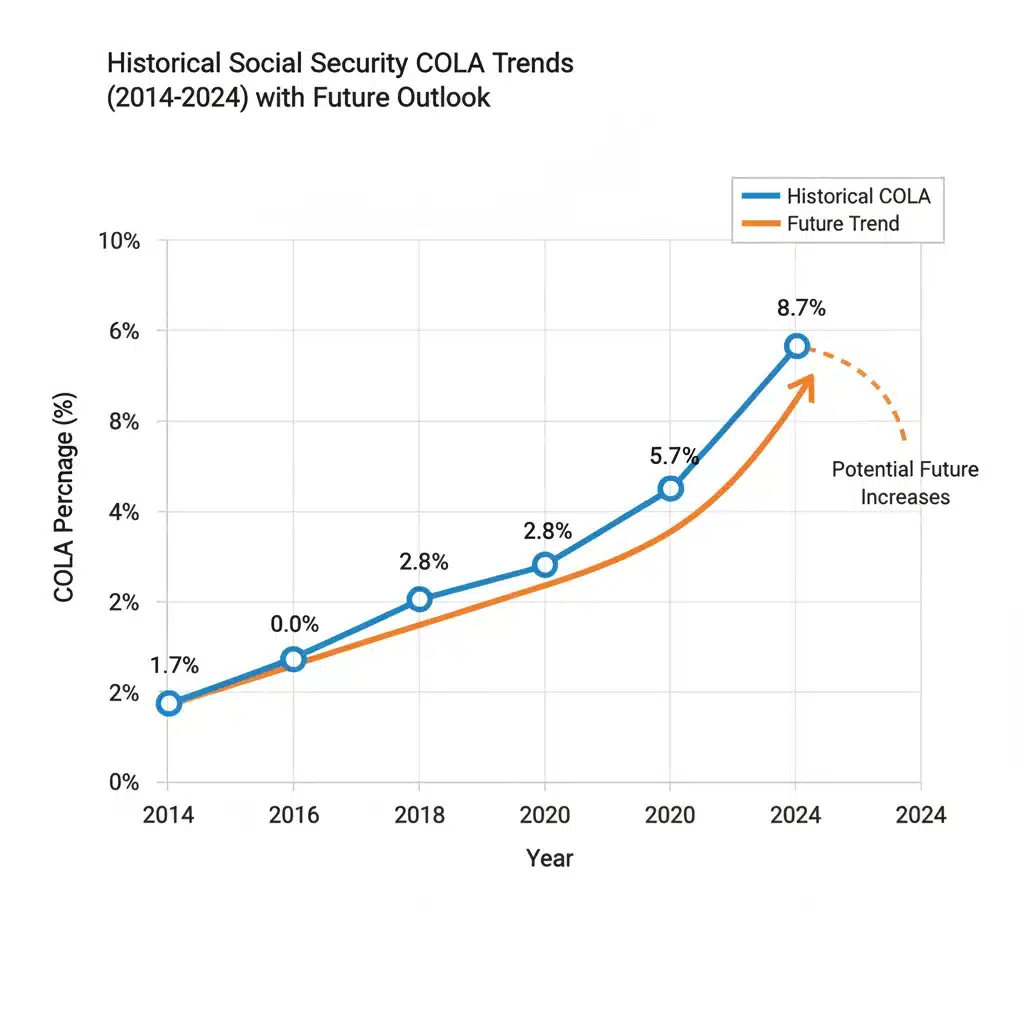

Historical COLA Trends and What They Tell Us

Examining historical COLA adjustments provides context and reveals patterns that can inform expectations for the future. Since its inception, COLA has varied significantly, reflecting different economic environments.

In the late 1970s and early 1980s, high inflation led to substantial COLA increases, with some years seeing double-digit adjustments. For instance, the 1980 COLA was a staggering 14.3%. This period was characterized by significant economic instability and high energy prices.

More recently, COLA adjustments have generally been more modest. There have been years with zero COLA, such as in 2010, 2011, and 2016, during periods of very low inflation or even deflation following economic crises. In contrast, the 2022 COLA saw a significant jump to 5.9% and the 2023 COLA to 8.7%, reflecting a surge in inflation driven by supply chain issues, pent-up demand, and geopolitical factors.

These historical trends demonstrate that COLA is not a fixed percentage but a dynamic response to the economic climate. While the specific percentage for the 2026 Social Security COLA remains unknown, understanding past fluctuations helps temper expectations and encourages proactive financial planning rather than relying solely on large annual increases.

Impact of the 2026 Social Security COLA on Your Retirement Planning

The 2026 Social Security COLA will have a direct and tangible impact on the monthly benefits received by millions of retirees. Here’s how it can affect various aspects of your retirement planning:

Increased Monthly Income

The most obvious impact is an increase in your monthly Social Security check. Even a modest COLA can translate into hundreds of extra dollars annually, which can be crucial for covering rising living expenses.

Maintaining Purchasing Power

The primary goal of COLA is to protect your purchasing power. If the 2026 COLA accurately reflects the rate of inflation, your benefits will be able to buy roughly the same amount of goods and services as they did before, preventing a decline in your standard of living.

Healthcare Costs (Medicare Part B Premiums)

A significant consideration for many retirees is Medicare Part B premiums. By law, if your Social Security benefit increases due to COLA, your Part B premium cannot increase by more than the dollar amount of your COLA increase. This ‘hold harmless’ provision protects many beneficiaries from seeing their net Social Security benefit decrease due to rising Medicare costs. However, this provision doesn’t apply to all beneficiaries, such as those who are new to Medicare, those who don’t have their Part B premiums deducted from their Social Security checks, or those with higher incomes subject to income-related monthly adjustment amounts (IRMAA).

Taxation of Social Security Benefits

It’s important to remember that Social Security benefits can be taxable. If your combined income (adjusted gross income + non-taxable interest + half of your Social Security benefits) exceeds certain thresholds, a portion of your benefits may be subject to federal income tax. A COLA increase, while beneficial, could potentially push you into a higher tax bracket or increase the taxable portion of your benefits, especially if your other income sources also grow. This is a critical factor to consider when estimating your net income after the 2026 Social Security COLA.

Overall Retirement Budget

When creating or adjusting your retirement budget, factoring in the anticipated 2026 Social Security COLA is essential. While you shouldn’t rely solely on COLA for significant financial gains, it’s a reliable component of income that should be accounted for. It helps ensure your budget remains realistic and sustainable in the face of inflation.

Strategies for Maximizing Your Social Security Benefits Beyond COLA

While the 2026 Social Security COLA is an automatic adjustment, there are proactive steps you can take to maximize your overall Social Security benefits and ensure a more secure retirement.

Delaying Claiming Benefits

One of the most impactful strategies is to delay claiming your Social Security benefits beyond your earliest eligibility age (62). For each year you delay claiming past your full retirement age (FRA) up to age 70, your benefits increase by approximately 8% per year. These delayed retirement credits are permanent and result in a significantly higher monthly payout for the rest of your life. This higher base benefit will then be subject to the annual COLA, further amplifying the impact of the 2026 Social Security COLA and subsequent adjustments.

Working Longer

Your Social Security benefit is based on your 35 highest-earning years. If you have fewer than 35 years of earnings, or if your current earnings are higher than some of your past earnings, working a few more years can replace lower-earning years with higher ones, boosting your average indexed monthly earnings (AIME) and thus your benefit amount.

Understanding Spousal and Survivor Benefits

If you are married, divorced, or widowed, you may be eligible for spousal or survivor benefits. These can sometimes be higher than your own earned benefit. It’s crucial to understand these rules and coordinate claiming strategies with your spouse to maximize benefits for both individuals.

Reviewing Your Social Security Statement

Regularly review your Social Security statement, which you can access online through your My Social Security account. This statement provides an estimate of your future benefits and details your earnings record. Check for any errors in your earnings history, as these could negatively impact your future benefits. Correcting errors now can ensure your 2026 Social Security COLA is applied to the correct base amount.

Consulting a Financial Advisor

Navigating the intricacies of Social Security and retirement planning can be complex. A qualified financial advisor specializing in retirement can help you develop a personalized strategy, considering your unique financial situation, health, and longevity expectations. They can model different claiming scenarios and help you understand the long-term implications of your decisions, including how COLA adjustments will factor into your overall plan.

The Broader Economic Picture and Future COLA Projections

While we eagerly await the announcement of the 2026 Social Security COLA, it’s beneficial to consider the broader economic context and what it might mean for future adjustments.

Inflation Outlook

Economists and central banks are constantly monitoring inflation. Factors like global supply chain stability, energy market dynamics, labor market conditions, and fiscal policies will all influence the inflation trajectory. A return to sustained high inflation could lead to larger COLA increases, while a period of disinflation or stable prices would likely result in more modest adjustments.

Social Security’s Long-Term Solvency

It’s also important to acknowledge discussions surrounding the long-term solvency of the Social Security trust funds. While COLA is an integral part of the program, debates about potential reforms (e.g., changes to the retirement age, adjustments to the COLA calculation method, or modifications to the benefits formula) occasionally surface. These discussions, while not directly impacting the 2026 Social Security COLA calculation, are part of the ongoing dialogue about the program’s future. Staying informed about these broader policy debates is a component of comprehensive retirement planning.

Healthcare Costs and Their Influence

As mentioned, healthcare costs are a significant concern for retirees. Even if the overall COLA is modest, if healthcare inflation outpaces it, retirees may feel a squeeze on their budgets. This underscores the importance of having a robust healthcare strategy in retirement, including understanding Medicare options and potential out-of-pocket expenses.

Preparing for the 2026 Social Security COLA Announcement

As the time for the 2026 Social Security COLA announcement approaches in October 2025, here’s how you can prepare:

- Stay Informed: Follow economic news, particularly reports on inflation and the CPI-W. Reputable financial news outlets and the Social Security Administration’s official website are excellent resources.

- Review Your Budget: Revisit your retirement budget and identify areas where rising costs might be a concern. This will help you understand how any COLA adjustment, large or small, will impact your spending power.

- Consider Other Income Sources: Evaluate how your other retirement income sources (pensions, 401(k) withdrawals, investments) might interact with your Social Security benefits and any COLA increase.

- Assess Tax Implications: If you anticipate a significant COLA or have other income changes, consider how it might affect the taxation of your Social Security benefits. Consulting a tax professional can be beneficial.

By taking these proactive steps, you can ensure that you are well-prepared for the 2026 Social Security COLA and can adjust your financial plans accordingly.

Conclusion

The 2026 Social Security COLA represents a vital adjustment designed to protect the purchasing power of retirees’ benefits against inflation. While its exact percentage won’t be known until late 2025, understanding the calculation methodology, historical trends, and influencing economic factors is crucial for sound retirement planning. By staying informed, proactively managing your finances, and exploring strategies to maximize your benefits, you can navigate the future with greater confidence and ensure your Social Security income continues to support your desired retirement lifestyle. Social Security is a cornerstone of financial security for millions, and comprehending its nuances, including the annual COLA, is an empowering step towards a well-planned and comfortable retirement.

Contribution Limits: Maximize Your Retirement Savings")

Contributions 2025: Maximize Your Growth")

Limits & Smart Moves")